Risk Management: Time to Get Real

In late June, Waters hosted a webcast on the topic of real-time risk management, sponsored by Misys and SAP, during which a number of issues and challenges were addressed. The perennial challenge of defining what exactly capital markets participants mean when they use the catch-all term “real-time risk management” proved contentious, leading the webcast panel to conclude that its implications differ from firm to firm, depending on their investment strategies and horizons, and risk management techniques and requirements.

Also of interest was a discussion drilling down into the specific technology “ingredients” required to build the ideal real-time risk management framework applicable to today’s market participants. Panelists included Sanjay Sharma, chief risk officer, global arbitrage and trading, at RBC Capital Markets; Marat Molyboga, chief risk officer, director of research, at Efficient Capital Management; Ted Luchsinger, financial services industry principal at SAP; and Thomas Moser, product manager at Misys. Victor Anderson, editor-in-chief of Waters and WatersTechnology, moderated the discussion.

Proactive and Reactive

Sharma is chief risk officer, global arbitrage and trading, at RBC Capital Markets, which trades 12 global master strategies around the clock, incorporating approximately 40 algorithmically driven sub-strategies underpinning the firm’s arbitrage business.

“To us, real-time risk management means the ability of our systems to react to market events,” Sharma says. “You might have real-time risk management in normal trading days where the movements are less than 1 percent, and during those conditions, markets are predictable and real-time risk management is something that you have a good feel for.”

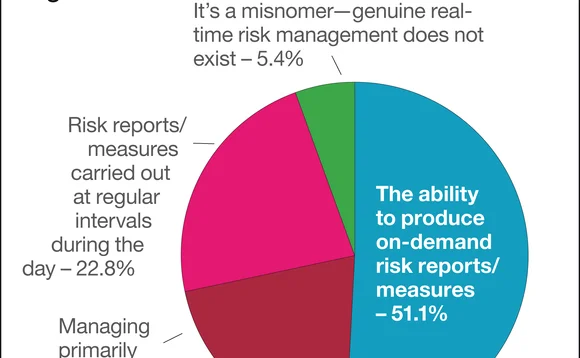

According to Sharma, the real test of his firm’s real-time risk management abilities occurs when there are volatile and unpredictable market movements and it needs to decipher what is happening in the market while trades—executed at high frequencies via algorithms—are being fired into the marketplace. “Real-time risk management is not necessarily a measure or a position,” Sharma says. “It is daunting indeed, and it applies very well to markets that are coded continuously, but not necessarily to other types of securities like credit or non-investment-grade bonds or more complex securities like mortgage-backed or asset-backed securities and collateralized loan obligations, that do not contain identical instruments coded in real time.”

“The deals we’re setting up have relatively broad risk limits on a pre-trade basis—that is where we try to implement broad identification management of potentially excessive risk exposures. When I identify an excessive risk exposure, that’s when we will take action.” —Marat Molyboga, Efficient Capital Management

Molyboga, chief risk officer and director of research at Efficient Capital Management, a Chicago-based multi-asset manager in the managed futures space, is responsible for all aspects of risk management at the firm, including portfolio and enterprise risk management. Efficient Capital Management currently invests in 35 commodity trading advisors (CTAs), exclusively through managed accounts, which, according to Molyboga, is important because managed accounts provide full control and transparency of trades and positions along with a complete and accurate view of exposures at the end of each trading day.

“When I think of risk management, I think of two components,” Molyboga says. “Sanjay talked a lot about the reactive component, but I’d also like to mention the proactive component. The deals we’re setting up have relatively broad risk limits on a pre-trade basis—that is where we try to implement broad identification management of potentially excessive risk exposures. When I identify an excessive risk exposure, that’s when we will take action.”

Molyboga says that in the managed futures space, clients are typically comfortable with a one-day delay in risk exposure calculations, because the investment horizon is a relatively long way off and large positions are built up over weeks or even months. In addition to that, he says, there is also an inherent limitation of give-up agreements. “For example, if a CTA executes through an executing broker and then gives up the trade to the prime broker, that position is not known with certainty until after the market settles,” he says. “Therefore, intra-day updates of positions provided by prime brokers or futures commission merchants (FCMs) are incomplete. To overcome that, we work toward getting direct updates from CTAs and reconcile those with prime brokers, which helps with real-time risk monitoring.”

Ideal System

According to Moser, product manager at Misys, the technology is already available to market participants to manage their risk on a real-time basis, although, as with a number of other facets of the capital markets like big data management, customer relationship management (CRM), and client reporting, firms have been slow to fully embrace it.

“The technology is available and is being used in a number of other industries to do much more than we are asking it to do for financial risk management,” Moser says. “The task for us, as vendors, is to enable banks and investment firms to employ this technology, even though they are not starting from scratch—they have legacy systems in place and we need to design our systems in a modular way so that they can be deployed step-by-step, helping clients move from the current state of risk architecture to one that possesses all the ingredients to do real-time risk in various flavors.”

According to Moser, any real-time risk management framework must boast four components: “From an architecture perspective, you need to be able to distribute your calculations; you need the ability to intelligently decide how and when to react when distributing these incidents through the use of complex-event processing (CEP) technology so that you don’t have to process your entire book all the time; you need a pricing engine that ideally includes a mix of central processing units (CPUs) and graphics processing units (GPU); and finally, you need a fast, real-time aggregation engine. The answer is to do that in-memory and there are different technologies available to do that.”

Luchsinger, financial services industry principal at SAP, says he agrees with Moser’s assessment, but stresses the importance of any system’s flexibility, given the industry’s propensity for change, especially when it comes to risk management and regulation. “A couple of terms that have come up so far are ‘flexibility’ and ‘agility,’” Luchsinger says. “The reality is that whatever system you’re building today to deal with risk measures—that’s going to change. The only constant in this industry is that things are changing. One of the things we haven’t spoken about today is confidence levels in inbound data going into firms’ models. If the inbound data is not accurate or they don’t have high confidence levels in it, then the numbers they’re going to come up with are a guesstimate at best.

Luchsinger says he agrees with Moser regarding in-memory data processing as the key to providing market participants with faster, more accurate data analysis, which, he says, has already been around the capital markets for a number of years. “I think you also have to add a predictive component to it, although I think the ideal risk management application of tomorrow hasn’t been written yet—a lot of the parameters are still changing,” Luchsinger says. “When you look at the Office of Financial Research (OFR), part of the Dodd–Frank realignment, we’re going to see regulators using analytics and streaming data to analyze markets and demand stress-tests. Stress-testing is crucial and an in-memory environment where the data and processing are co-located is the way to effectively start stressing your data and understanding what your volatility is on a real-time, continual basis.”

Only users who have a paid subscription or are part of a corporate subscription are able to print or copy content.

To access these options, along with all other subscription benefits, please contact info@waterstechnology.com or view our subscription options here: https://subscriptions.waterstechnology.com/subscribe

You are currently unable to print this content. Please contact info@waterstechnology.com to find out more.

You are currently unable to copy this content. Please contact info@waterstechnology.com to find out more.

Copyright Infopro Digital Limited. All rights reserved.

As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (point 2.4), printing is limited to a single copy.

If you would like to purchase additional rights please email info@waterstechnology.com

Copyright Infopro Digital Limited. All rights reserved.

You may share this content using our article tools. As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (clause 2.4), an Authorised User may only make one copy of the materials for their own personal use. You must also comply with the restrictions in clause 2.5.

If you would like to purchase additional rights please email info@waterstechnology.com

More on Trading Tech

APAC’s hidden opportunity is in the hands of wealth managers

Asia-Pacific’s financial firms have lofty growth ambitions that will come with high cost and complexity. To succeed, they’ll need a quality portfolio toolkit and a connected technology architecture, writes BlackRock’s James Verner.

Apac buy-side firms embrace AI and automation to bolster the business

How Apac buy-side firms are using AI, APIs and automation to transform investment workflows

TMX to undertake extended trading hours in Canadian equities

Exchange operator looks to keep pace with US markets and potentially undercut Canadian competitors.

Pimco replaces Bloomberg EMS with TS Imagine

Fixed income giant is shrinking its Bloomberg EMS footprint, though not removing it completely, sources say.

24X says requested SIP exemption won’t break the market

In a new letter to the SEC, the startup exchange says data infrastructure that operates like the SIP is available as it looks to launch overnight trading this summer.

What firms get wrong when changing investment operations technology

Without operating redesign, governance, and clear accountability, modernization can amplify risk instead of reducing it, writes Patrick Conroy.

In record year, SS&C changes division name, emphasizes role of AI

Announcing the vendor’s record financial results, CEO and chairman Bill Stone reassured investors that the vendor is not depending too heavily on AI.

Cboe sells to TMX, TT links to NZX, Broadridge and Digital Asset invest in HQLAX, and more

A recap of this week’s major tech and data news in the capital markets.